Fund Size as a Strategy

At Moonfire, how we think about fund size and portfolio construction is just as important as picking our investments.

Here at Moonfire, how we think about fund size and portfolio construction is just as important as picking our investments. Of course, we spend a lot of time thinking about how to pick winners and we use a data-driven approach (building a bionic VC) to aid our sourcing, evaluation, decision making and scaling. We also use data and software to help evaluate our fund size and portfolio construction.

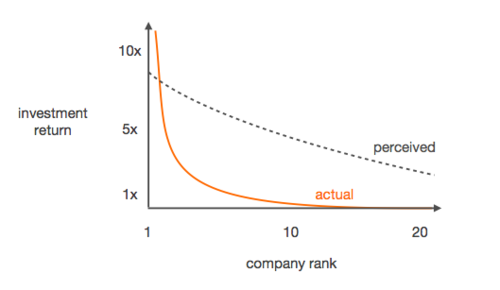

Tech investing is affected by the power law distribution where your best investment is worth more than your whole fund while the returns from your next best investment is half as impactful and so on. This accepted wisdom defines the industry we are in.

Portfolio Diversity

The power law distribution also impacts how we think about our fund size to balance portfolio diversity and ownership goals. A fund needs to be big enough to allow you to obtain diversification (shots on goal) that have the potential to be unique outliers (home runs). However, we also need to achieve ownership levels that let the magnitude of the biggest exit have enough impact to drive that outsized return.

Deciding on a specific fund size for a seed fund determines the level of diversification and ownership we can achieve. With our Fund I we aim to make 30-35 investments. This should allow us to get significant ownership, be sufficiently diversified and return funds to our LPs within a reasonable time.

Portfolio Allocation and Construction Drive Returns

To understand the number of possible investments your fund can make you need to set a strategy on the amounts that you want to invest. For our core and non-core investments we plan completely without recycling of management fees (for more on this read Brad Feld post here). This gives us a good understanding of the number of investments we should plan to do. Our follow-on reserves can then potentially be topped up with recycling and thus the number of follow-ons can vary.

Investing 100%, or even more, of the entire fund is not straightforward and requires planning.

Getting Recycling Right

Recycling can allow you to invest more than 100% of the fund. To do so you need to have some early returns/exits, which is generally more difficult for early-stage funds because (significant enough) returns, compared to later stage investments, tend to materialise later and hence might be available too late.

Understanding your Loss Ratio

In venture capital, you expect to have investments that are lost, some that break even and some that drive outsized fund returns. If you set out to minimise fund losses, you are likely not taking enough risks and it is also not recommended to place your bets on only a few companies. At Moonfire, we strive to focus on our core investments while we monitor our non-core investments closely to be ready to convert these into a core investment, if appropriate. Our target is for one third of our core investments to become winners and that one of those should more than pay back the fund.

Ownership is Key

It is important to understand what your investments buy you in terms of ownership. You can do many investments aiming for relatively low ownership or fewer investments that buy you more ownership. Both the entry-ownership and the exit-ownership are important and thus the dilution from the subsequent investment rounds. All these assumptions allow you to calculate enterprise values for which the companies should be sold in order to return the fund.

Continue to Model your Outcomes Scenarios

We have a clear fund model but that does not stop us from using our model to test the sensitivity of our assumptions. It’s easy to forget the impact of decisions if you move outside your model. By plugging in different scenarios we see clearly what our new assumptions have to be. With an ever changing world it’s important to reinforce your north star.

🌗 🔥

This post was co-authored by Mattias Ljungman and Nico Caprez.

Special thanks for the inspiration to Mike Maples, Peter Thiel, Roelof Botha, and Paul Graham.